Issues dealing with Charitable Organisations

Few issues about Charitable Trusts

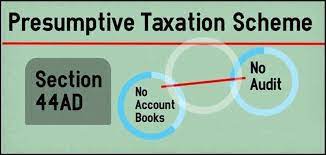

Presumptive taxation scheme was introduced in order to give relief to small taxpayers from complying with section 44AA and 44AB. The presumptive taxation scheme can be opted by the eligible persons, if the total turnover or gross receipts from the business does not exceed Rs.2 Crores. Presumptive taxation scheme of section 44AD can be adopted by the following eligible persons: